The Hamptons real estate industry was brimming with optimism for the third quarter back in July. Lackluster second-quarter figures were thought to be a result of long transaction periods between buyers and sellers, as they negotiated prices, and the hope was that a spate of closings was going to happen over the course of July, August and September.

But that didn’t happen.

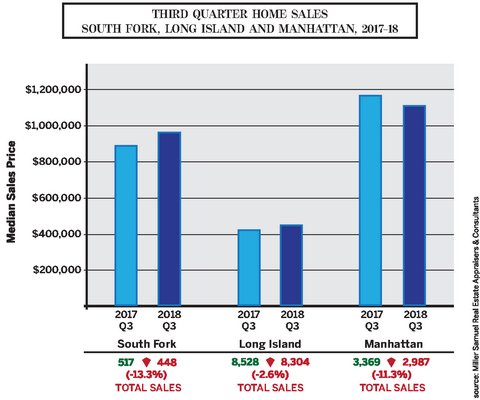

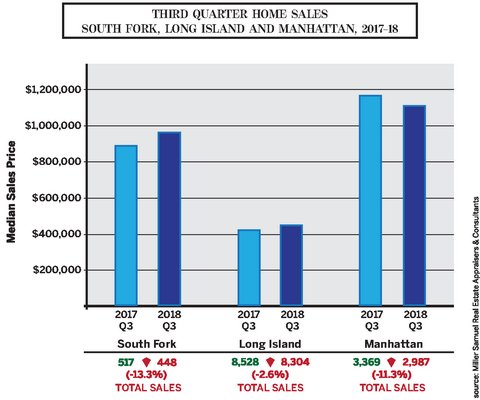

Instead, the number of South Fork home sales slipped by more than 10 percent for the third consecutive quarter year-over-year, according to area brokerages. The third quarter saw the worst decline, with a dip of more than 13 percent compared to the third quarter of 2017.

Homes priced between $1 million and $5 million had been the soft point for the second quarter. Now, both the low-end—homes prices below $1 million—and the high-end—luxury estates above $10 million—have fallen off. This caused the median home sale price for the South Fork to jump about $100,000 to $965,000.

Judi Desiderio, the CEO of Town & Country Real Estate, chalks the third-quarter results up to an unsettled Wall Street.

“There was quite a bit of momentum going into the third quarter,” Ms. Desiderio said. “But then the stock market did some gyrations and geopolitical events happened, and people took a pause.”

Jonathan Miller, the president of real estate appraisal firm Miller Samuel, which compiles quarterly reports for Douglas Elliman Real Estate, said Northeast markets have been depressed by a tax migration. That’s when homeowners in high-tax states, like Connecticut, are relocating to low-tax states, like Florida, to avoid significant tax burdens. Mr. Miller attributed recent tax migration to the new federal tax plan that was put into motion in April, which limited income-tax deductions for state and local taxes.

Carl Benincasa, a Douglas Elliman regional vice president of sales, said the buyer pool for the Hamptons market is largely Manhattan’s luxury homeowners; Manhattan had its own downturn at 11.3 percent fewer sales in the third quarter, year-over-year, of properties more than $5 million. The Long Island market, excluding the Twin Forks, has also seen a steady decline in home sales in recent years.

Mr. Miller said the Hamptons market is bucking the migratory trend seen elsewhere, because the success of the housing market on the South Fork is grounded in second-home owners.

“We never follow national trends,” Ms. Desiderio said. “But we are umbilically connected to Wall Street and run in patterns with Manhattan.”

Looking at the last decade in New York City, Ms. Desiderio speculates that developers overbuilt on the high-end in the Big Apple. Ms. Desiderio contends the South Fork won’t have that problem because it cannot support the same type of density with multi-unit buildings.

But the South Fork is experiencing its own version of the same problem. Inventory in the luxury market is the largest its been in the past decade: 452 compared to previous quarters in the mid-300s, according to the Douglas Elliman report. Mr. Miller attributed the rise to properties that have been pushed onto the market with the hope that there would be a buyer.

“It’s all about sales direction,” Mr. Miller said. “Because when sales slide—whether the rate of growth is slowed or a decline occurs—that leads to higher inventory, and then that leads to changes in pricing, which brings more competition. The whole process take about two years. Pricing is the caboose of the train. A lot has to happen before you can get to lower prices. And we are sort of in the middle of that process now where sales are easing and inventory is rising.”

As for the lower-end, the decline in sales can be attributed to a lack of inventory rather than a lack of buyer interest; as soon as a residence is put on the market, it’s scooped up.

“The slowdown in the sub-$1 million market, which was the engine of this year’s strongest segment of the market, shows that a lot of opportunities have already been taken advantage of in an ever-shrinking market,” Mr. Benincasa said.

Lawrence Ingolia, a global real estate advisor and associate broker at Sotheby’s International Realty, contends these buyers are hesitant because of climbing mortgage interest rates. “I have one client who is bouncing between banks trying to find a low rate, but he’s being offered 3.5 and 4 percent,” he said.

Also, according to Mr. Ingolia, homeowners on the low-end are less motivated to sell now and will wait for a more favorable market.

Mr. Ingolia said this contentious midterm election season hasn’t made buyers or sellers feel much better. During presidential election years, the market tends to dip in the third quarter as the country awaits new leadership. Midterms don’t typically have the same effect.

But the number of sales in the third quarter of 2018 was 17 percent lower than the same quarter during the last midterm election season in 2014, according to Sotheby’s. Sotheby’s also reported an even greater slip in the number of third-quarter sales between 2017 and 2018 than other brokerages reported: from 387 to 318, or 18 percent.

Contrary to third-quarter reports by Brown Harris Stevens and Douglas Elliman, Corcoran Group found that sales activity was up 1 percent on the South Fork. It’s report included 594 sales. “We capture every transaction so that transactions that were made in the second quarter that weren’t included in the second-quarter report are included into the third quarter,” said Ernest Cervi, Corcoran’s East End executive managing director.

The flat sales growth in the Corcoran report still showed people metaphorically sitting on the sidelines due to higher mortgage interest rates and an uncertain global economy, Mr. Cervi said. But he noted that could all blow over after the elections on November 6.

“It is time to take money out of Wall Street and put it in a property in the Hamptons,” he said. “Many homeowners are repositioning their pricing to be very competitive in this market. That signals to the buyers that there is an opportunity for value.”

BHS Executive Managing Director Cia Comnas said she sees a buyers’ market emerging in the Hamptons.

“I think a lot of the activity that was anticipated for the third quarter is really happening now—it got delayed a little bit,” Ms. Comnas said. “We are seeing first-time buyers coming into this market. The millennials are becoming of age, and entering the real estate market en masse. They, as buyers, are seeing price reductions every day, and sellers are getting used to the fact that it’s shifting to a buyers’ market.”

“The fall selling season has always been the most active selling season traditionally out here. Even though there are more people here in the summertime and properties look their best, it’s never really a transactional period because the homeowners are using them for the summer or renting them,” she continued.

As for what’s to come, Ms. Desiderio said she expects the fourth quarter of 2018 to be booming with bargain hunters in the dead of winter. These are people who made it big on Wall Street and know that sellers are looking to make a deal as properties languish on the market.

“That’s because certain segments of the market that were hit, frankly, have some incredible deals, especially if you are looking at the high end. If you bought the land, built the house and did the landscaping and the pool, you couldn’t come in at the price that some of these houses are at,” she said. “There is a lot of real value out there and today’s buyer, no matter what they are buying, they want to be buying value. The bargain hunters are going to be reaping some benefits.”

She’s eyeing south of Montauk Highway in Sagaponack and Bridgehampton, and East Hampton Village, as prime areas with valuable properties up for grabs. Those sales won’t show up until the first and second quarter of 2019 when deals close.

There is also an increased demand for more expensive homes with a better value in Westhampton, East Quogue and Hampton Bays for year-round residences, which offer an easier commute to New York City and the Twin Forks—seen as more bang for the buck.

JD Allen on Oct 26, 2018

JD Allen on Oct 26, 2018