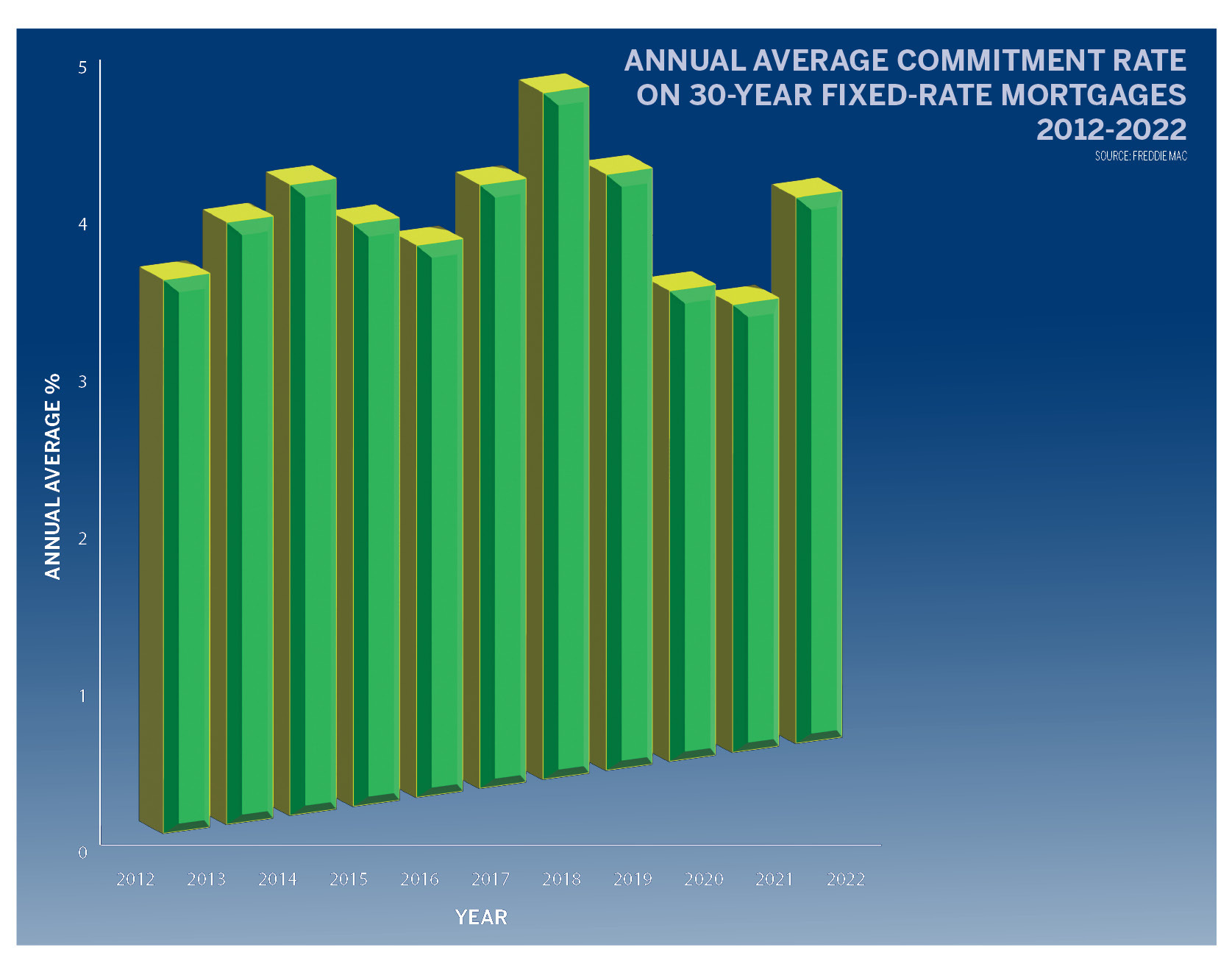

Average annual commitment rate on a 30-year fixed-rate mortgage from 2012 to 2022.

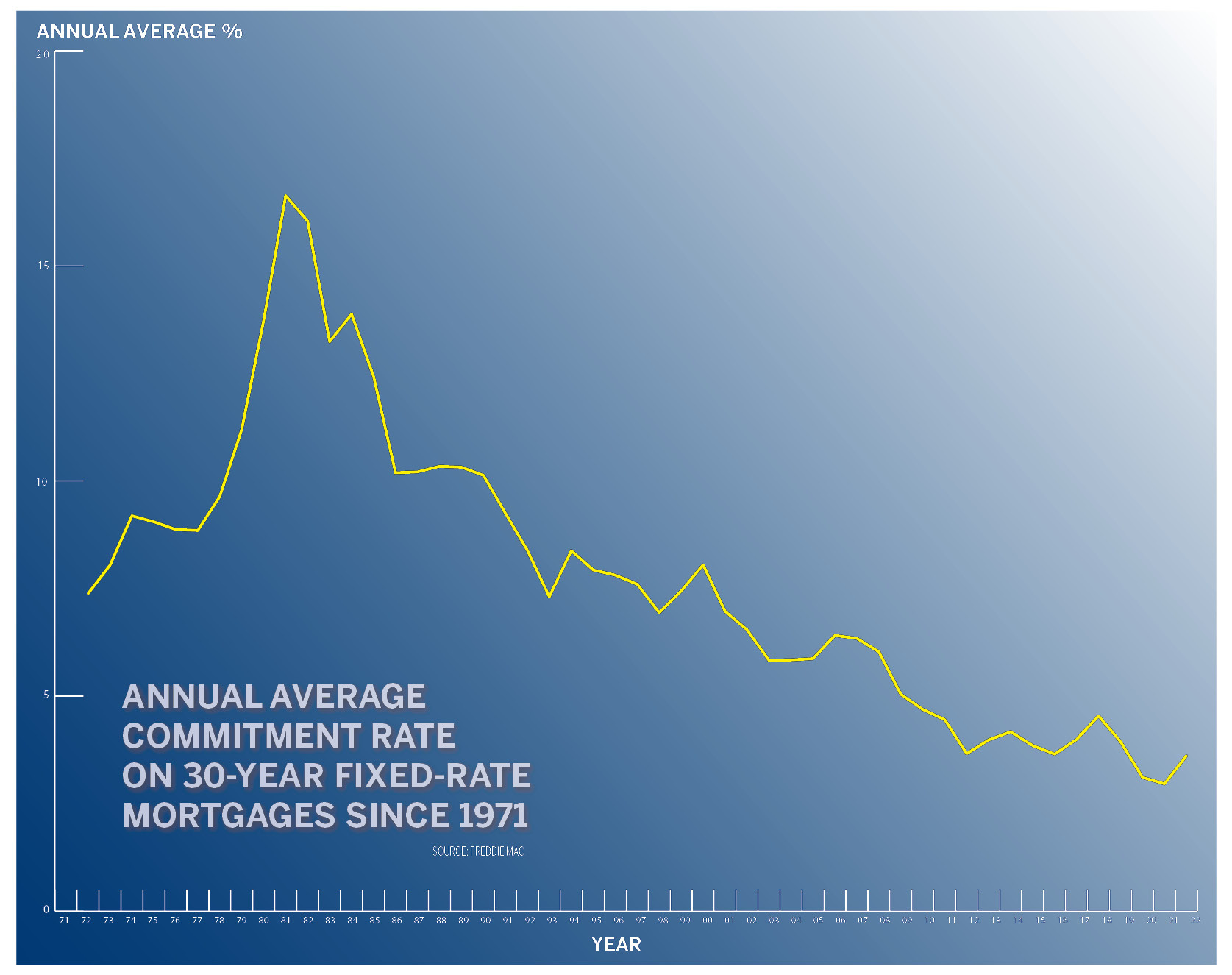

Average annual commitment rate on a 30-year fixed-rate mortgage from 1971 to 2022.

Even before the Federal Reserve nudged up interest rates last week, mortgages have only gotten more expensive — with the 30-year, fixed rate recently creeping above the 4 percent mark for the first time in three years.

But while ultra-low rates — like those seen in 2021, when 30-year loans were available for under 3 percent for most of the year, reaching a record low of 2.65 percent — are likely gone with the wind, experts say they don’t expect a major spike in rates in the coming year.

In fact, they say the Fed’s decision to tighten monetary policy will have little impact on the East End, where well-heeled buyers often buy second, third, or even fourth homes with cash. But it could shut out those first-time buyers already struggling to qualify for a mortgage, while facing high home prices and low inventory.

On March 16, Fed officials voted to raise the federal funds rate — the rate it recommends commercial banks charge for overnight loans to other banks — by a quarter percentage point to a range between 0.25 and 0.50 percent, marking the first increase since 2018.

But the Fed indicated it will make six similar increases over the course of the year, in an effort to tamp down inflation, which recently spiked over 7 percent after being virtually nonexistent for two decades. Although mortgage rates are more directly tied to the 10-year note rate, when the Fed tightens, it causes a ripple effect through the credit markets — raising rates on everything from savings accounts to car and home loans.

“Real estate values have gone up 25 percent nationwide in the last year, so it’s already hard for first-time buyers to afford a home,” said Judi Desiderio, president and chief executive officer of Town & Country Real Estate. “These rate increases may make it harder for renters to turn into buyers, or for first-time buyers to pull the trigger.”

Desiderio said she remembers the early 1980s all too well, when homeowners were forced to pay “18 and 19 percent.”

“So for me, anything under 10 percent is good,” she said, adding that shortly after the COVID-19 pandemic struck in March 2020, “The Fed pulled out every tool in its toolbox, including interest rates, to such a degree that I doubt we will ever see it again where you can get a mortgage for 2.5 percent.”

Still, she said, the impact of the Fed’s decision to begin tightening will have “a minuscule impact” on the East End, considering many buyers only took out mortgages because rates were so low, allowing them to keep the money they would have used to pay off a house invested in the stock market, she said.

Bill Wright, a partner at PAR East Mortgage in Southampton, agreed that the initial impact of higher rates would be felt by those “marginal borrowers,” who already had a hard time qualifying for a mortgage, when even a 1 percent increase can add a couple hundred dollars to their monthly payment. Although buyers can still obtain 30-year mortgages below 4 percent, the average is closer to 4.25 percent now that the Fed has signaled its intentions, he said.

“I don’t think we’ll see rates at 6 percent, but probably in the high 4s for a 30-year — maybe 5 percent,” he said, adding that he believes the market has already begun to price in further rate hikes by the Fed.

As long-term rates increase, some buyers may opt instead for adjustable-rate mortgages, Wright said, which typically offer discounted rates for the first few years before recalibrating to a higher rate. It is possible that persistently higher interest rates might temper the rise in house prices, he said, but that might take some time. Often, when rates start to increase, buyers rush to lock in, to avoid paying even higher rates, he said.

“The housing market has been insane for the past two years, where you’re seeing 20 to 30 people bidding on a house,” Wright said. “That market is going to die out.”

Still, he said, would-be home buyers should not expect the mortgage market to return to last year’s lows anytime soon. “I think this is the new normal,” he said. “I think it’s the end of ultra-cheap mortgages — for a while.”

Nancy Tomich, the executive vice president for residential and consumer lending at Dime Community Bank, said she was too cautious to call the recent lows in mortgage rates a generational low.

“We all see different cycles, so I always hesitate to say this will never, ever happen again,” she said, though if rates fall below 3 percent, it will signal that the economy is in bad shape.

The recent uptick in mortgage rates does not come as a surprise, according to Tomich. “There’s been a lot of talk and predictions that rates were headed north” going back to early last year, she said. “During the pandemic, rates were intentionally left low. But with inflation back at 7 percent, the Fed is really determined. They want it back to 3 percent.”

Tomich said she expects to see 30-year rates stay comfortably above 4 percent for much of the next year, but added that there are many variables, from the Russian invasion of Ukraine to the volatile prices of commodities, like oil and grain, that could have an impact on where rates end up.

“The first-time home buyers are the ones who feel these types of changes,” she said of increasing rates. “Sometimes higher rates help drive down prices, but with such low inventory, it is going to be interesting to see what that time frame is.”

Rising rates will make an already difficult East End real estate market even more problematic for middle class buyers, who face a huge challenge in finding homes for less than $1 million, according to Dawn Watson, a licensed real estate salesperson with Douglas Elliman Real Estate in Westhampton Beach.

“It creates an inequity that will only grow bigger and bigger,” she said. “The wealth divide, I fear, is going to get more expansive.”

Watson reported she recently sold a three-bedroom, one-bath house for $710,000 — “a regular person’s house to a regular person couple,” she said, “and that regular person couple sold their car to help with the down payment.”

“I was happy,” she continued, “because the seller took the money and will move out of state and be able to buy a house for under $300,000, and have money left over to retire on.”

Still, she said, it was a double-edged sword. “I hate to see you go, but I’m happy to see you go,” she said.

Stephen J. Kotz on Mar 22, 2022

Stephen J. Kotz on Mar 22, 2022