Credit card companies charge lower fees to merchants when customer inserts a chip card into a reader than it does for phone app charges or online ordering, because of the lower risk of fraud in transactions that use the physical card.

Many business have started informing customers of fees charged for use of credit cards when the get to the counter. A state law implemented in February states that the fees have to be incorporated into the price of the item, or two prices shown.

Many business have started informing customers of fees charged for use of credit cards when the get to the counter. A state law implemented in February states that the fees have to be incorporated into the price of the item, or two prices shown.

Many business have started informing customers of fees charged for use of credit cards when the get to the counter. A state law implemented in February states that the fees have to be incorporated into the price of the item, or two prices shown.

The credit card surcharge has crept into daily life like rust on a tractor — appearing so slowly that customers hardly notice it until it is, seemingly, all over.

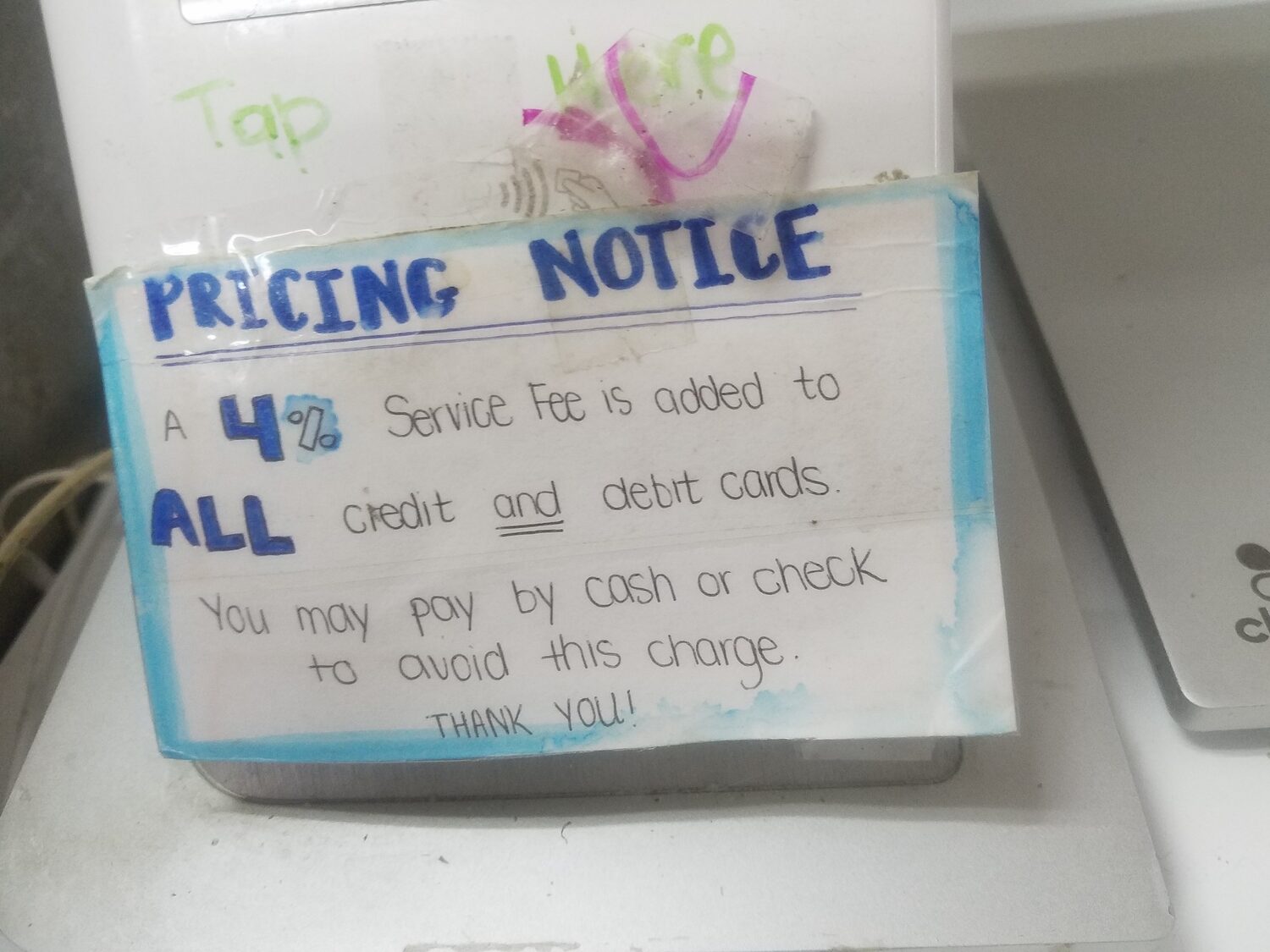

The little signs on cash registers announcing, or acknowledging, that a surcharge of up to 4 percent will be added to the price of any transaction that is paid for with a credit card bother some consumers more than others, but everyone has noticed them.

The card surcharges have become most common at places like delis and small markets and modestly priced retail stores. They’re less common but not unheard of at some restaurants. No large grocery or department store chains tack them on — yet — and few of the high-end shops on the main streets of South Fork’s hamlets bother with them.

It is “legal” for stores to charge credit card fees to customers — in case you were wondering, or thought otherwise — and has been for more than a decade.

But last winter, the State Legislature and Governor Kathy Hochul approved a new law requiring that merchants do so in a very different way than almost any stores do currently.

The new approach, in effect since February, has left some merchants scratching their heads, others crying foul, and some persnickety consumers howling that they are being wronged by business owners who have not yet complied with the new requirements.

“There’s two things at the heart of the rule: merchants and vendors can’t charge more of a surcharge than they are being charged by the credit card companies themselves, and the other is this idea that the consumer has to be aware before they decide to purchase the item what the total price, including the surcharge, would be,” said Assemblyman Fred W. Thiele Jr., who ultimately voted in favor of the bill.

“The debate over the law at the time was between the consumers’ right to know the full price of what they are paying for and not be surprised afterward, and the burden put on small businesses by this — and what some think is an anti-business climate in New York State.”

For decades, passing on the fees that credit card companies charged to merchants to the consumer was, in fact, not allowed — by the card companies themselves. A 2012 class-action lawsuit by business interests against Visa and Mastercard, changed that.

Starting in 2013, merchants nationwide were allowed to tack on a surcharge for consumers using credit cards for purchases to cover the fees the business would be charged. Most states required that they inform the customer of this, which was done most commonly with the small signs now ubiquitous at checkout counters across the South Fork.

One of the first applications of the new rule was at gas stations, which have been displaying two prices for years, one the cash price and the other the price for paying with a credit card — an approach that allowed them to still advertise their best per-gallon price but to get more when someone paid at the pump.

Typically, the stations will charge about 10 cents more per gallon — which can be considerably less than what they are paying in fees, depending on the price of a gallon of gas, but doesn’t stress the bounds of what customers may be willing to write off for the convenience of not having to go inside to pay cash.

And the way gas stations have displayed how they offset credit card fees is much like what New York State says all merchants must do with their pricing announcements.

The law requires that the credit card surcharge be incorporated into the price of the item wherever it is displayed to the customer: either showing two prices — one with the fees and one without — or just the single higher price, and then the customer can be informed at the register that there is a discount for cash payment.

The system is a nonsensical and costly headache the stated intentions of which are poorly conceived, say many store owners faced with figuring out how to implement it.

“First of all, it would probably take a month’s worth of man hours to go through the 150,000 individual items in the store and reprice everything. Who pays for that?” said Bryce Poyer, owner of White Water Outfitters, a fishing tackle retailer in Hampton Bays.

“Secondly, putting two price stickers on an item would be way too confusing. And there’s still tax to be added on, so how are you helping the consumer? You’re saving them doing the math on the 3 percent before they bring an item to the counter — but they still have to do it for the 9 percent in tax?”

Poyer said he thought the way merchants are doing it now — he only started tacking on a credit card surcharge this past winter — is perfectly reasonable. Perhaps more clear signage in the store informing customers of the surcharge would be a sensible compromise, he said, but to impose financial losses on a business simply to save someone making a simple calculation in their head seems excessive.

“And everybody has a calculator in their pocket,” he noted.

Some business owners who were adding a card surcharge have given up passing on the fees out of frustration and returned to eating five- and six-figure annual bites out of their bottom line for fees.

“We did it for maybe six months last year and early this year — a lot of places started doing it after COVID just to keep up with all the additional fees because nobody was using cash,” Southampton Publick House owner Donald Sullivan said. “But then it just became a point of confusion. The last thing you want is for people to be annoyed at the end of their meal.”

When the state adopted the new requirements for displaying the pricing, Sullivan abandoned the surcharge rather than tackle the more complicated pricing or raise his prices when his competition was not.

“Credit card usage is 96 to 97 percent, so, do the math: It’s costing me $100,000 a year to pay for credit card fees — that’s a hell of a lot of money.”

He is not alone in that sentiment.

“We struggled with it and some of my employees got verbally abused for it, so we stopped,” Steve D’Angelo, owner of North Sea Hardware said. “I was told that in order to do it, you have to tag everything with both a cash price and credit card price. That might be doable for some retail businesses that have limited inventory, but it’s not feasible for a hardware store. So we just gave it up — it was too much.”

The state’s approach, he added, will more likely just mean that eventually, as the new rule gets worked into the system, all consumers will pay higher prices as merchants build the costs of credit card fees into the pricing and don’t offer the discount for cash to the rare customer who whips out greenbacks.

“If someone is paying $10,000 a month in credit card fees, that’s going to have to come from somewhere,” D’Angelo said. “There’s a lot of low-margin items out there … because there are national brand name products that if you take 3 percent off, we’re only maybe breaking even on them. The town asks us to sell their garbage bags, but we aren’t allowed to make money on them, so if someone comes in and buys them with a credit card, I literally lose money on that transaction.”

“Nobody pays with cash anymore,” D’Angelo said. “Even for something that’s $2, they hold their Apple watch up to the thing and, ding, they’re gone.”

A spokesperson for the Department of State Bureau of Consumer Protection said that the point of the law was so that people were not caught by surprise when they paid for something with a credit card. The signs at the register that most stores have employed, were not sufficient in the eyes of those looking out for consumers, she said.

“The very broad intention was that the consumer know these fees before they decide to purchase something, so you’re not going to find out when you get to the register,” Deputy Secretary for Public Affairs Michelle Rosales said. “We don’t want customers to be surprised.

She acknowledged that the state’s 8.625 percent sales tax is still looming with every purchase, and a considerably more complicated calculation to do in your head, is not addressed.

“Tax has been around forever and people know to expect it,” she said. “The consumer protection is simply ensuring people are aware of the impact of potential surcharges on their purchases.”

Business owners also pointed out that the fee charged to merchants by the credit card companies varies by up to 2 percent, depending on the type of transaction and depending on the credit card company — an impossibly convoluted calculation. That means the cost of an item calculated to include a credit card surcharge could not possibly accurately reflect what the actual fee charged for each individual purchase of that item will end up being.

When a customer pays at the register with a card in their hand, the fees charged by the card companies are the lowest — typically less than 2 percent. Payments through mobile phone apps are a bit more. If a card number is punched in manually — like for a house account charge — that’s even more.

If a card number is entered but a CVC code is not, the fee will go up another fraction of a percent more. Online purchases carry the highest fees to merchants, up to 3.5 percent, because the risk of fraud they must assume is much higher.

Some frustrated policy hawks who are especially irritated by the fees have pointed out that most stores are still imposing the surcharges the old way, and that there has been zero enforcement of the new requirements.

“To punish a consumer for using his credit card by local vendors amounts to a [double charge] as consumers pay a fee to the company for the use of their credit card and therefore for a vendor to charge a fee for its use is extortion,” said Michael Griffith, and East Hampton resident who has raised a fuss over the surcharge policies at many stores this summer. “Why would a person possibly want a credit card under these circumstances?”

Griffith has expressed frustration that his numerous complaints to local authorities have not resulted in a crackdown on offending businesses.

The state law, like all state business law statutes, puts responsibility to enforce the laws to the state attorney general’s office but allows local municipalities at the town and county level to enforce them if they see fit.

Local towns say that they are looking at the impacts of the new law and considering whether or how they can steer businesses toward compliance. For the time being, they are directing complaints to the New York State Attorney General’s office, or to Suffolk County Bureau of Consumer Affairs.

In Southampton Town, Councilwoman Cyndi McNamara said that the town has no specific plans for enforcing the state statutes, preferring to leave it to the state or Suffolk County Consumer Affairs to handle complaints.

McNamara said she didn’t personally see the state’s new approach as being very effective in helping consumers.

“If we’re doing this so people know what they are paying, but then they have to figure out how much less it would be if they pay cash, and they still don’t know how much the tax is — what are you accomplishing here?” she wondered. “I see what they wanted to do, but this just makes no sense.”

Michael Wright on Sep 4, 2024

Michael Wright on Sep 4, 2024